Buying your first home is thrilling, but it can feel overwhelming without proper guidance. From selecting the right location and property type to understanding loans, taxes, and other financial benefits, every decision counts. This guide walks first-time homebuyers through the entire process, offering practical tips on budgeting, legal checks, and documentation.

It also highlights common pitfalls to avoid and ways to maximise your investment. With clear, step-by-step advice, first-time homebuyers can feel confident, prepared, and empowered, turning what can be a stressful experience into a smooth and rewarding journey toward homeownership.

Here are some important steps to follow when buying a house for the first time:

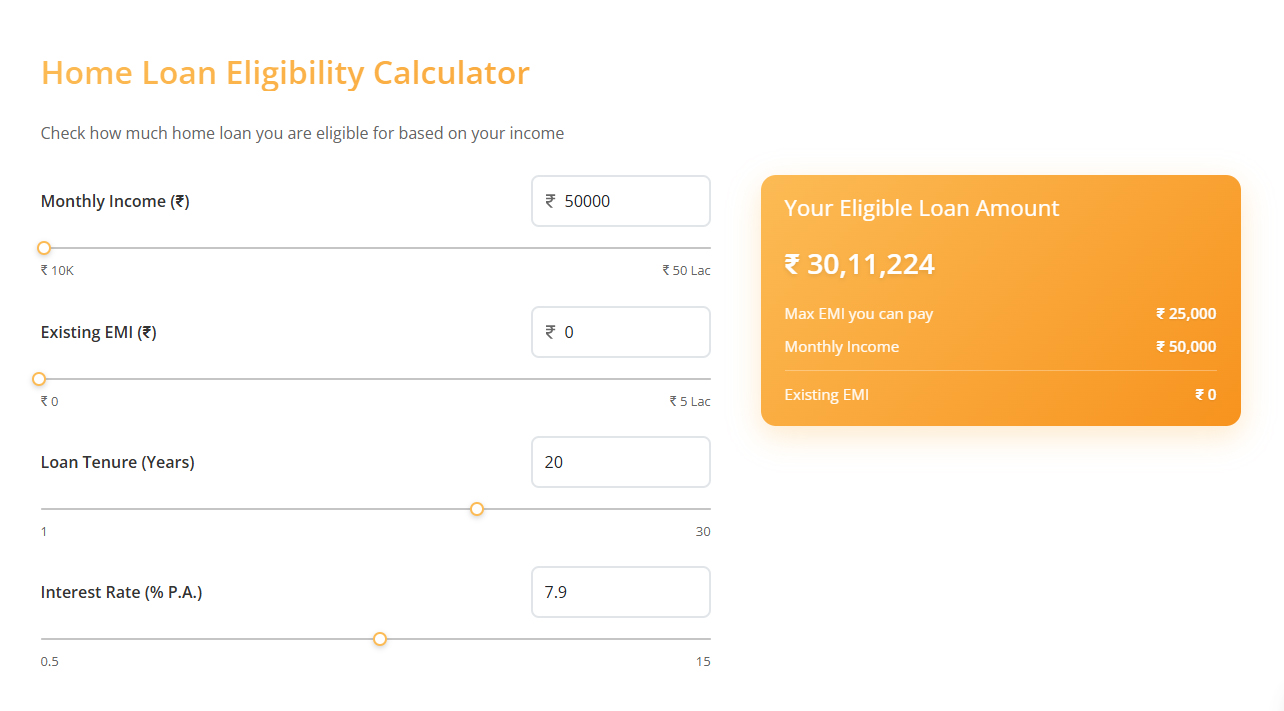

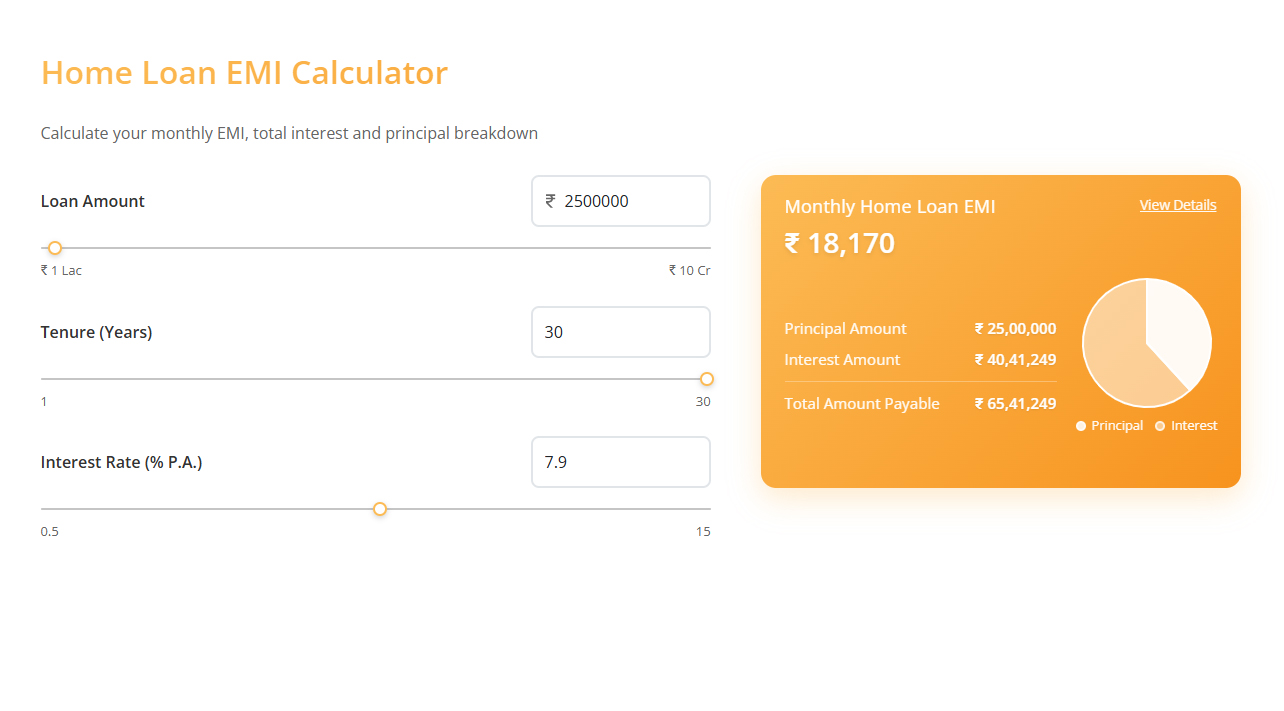

A first-time homebuyer loan is designed for new buyers entering the property market. Here’s what to know:

First-time homebuyers in India can enjoy several tax benefits under the old tax regime:

Note: Under the new tax regime, only interest on home loans for let-out properties is deductible.

Even with excitement and careful planning, first-time homebuyers can stumble on avoidable missteps. Here are some common mistakes to watch out for when buying your first home:

Buying your first home is an exciting milestone. By understanding first-time homebuyer benefits, loans, tax deductions, and the buying process, you can make informed decisions and enjoy a smooth homeownership journey. Planning carefully ensures financial security and long-term peace of mind.

First-time homebuyers can enjoy lower interest rates, access to special loan schemes, tax deductions on principal and interest payments, and government incentives designed to make homeownership more affordable.

You will need identity proof (like Aadhar or PAN), address proof, income proof (salary slips or IT returns), bank statements, and property-related documents such as the sale agreement and title deed.

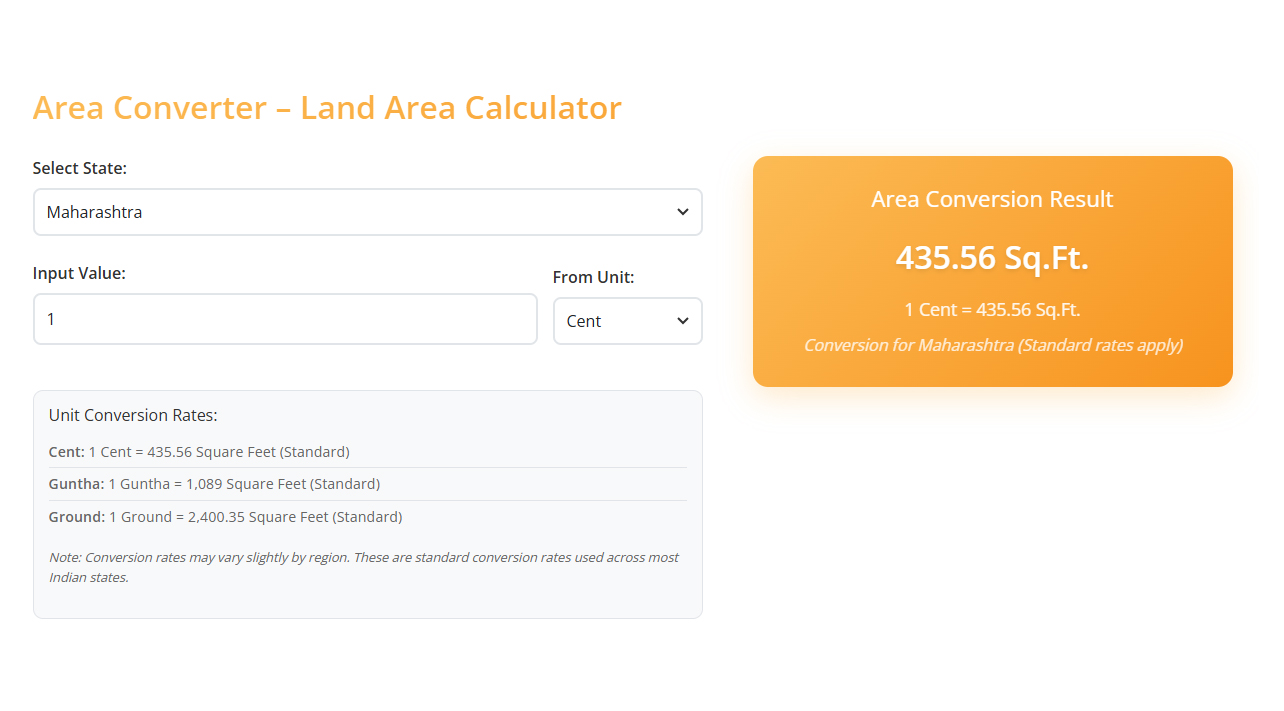

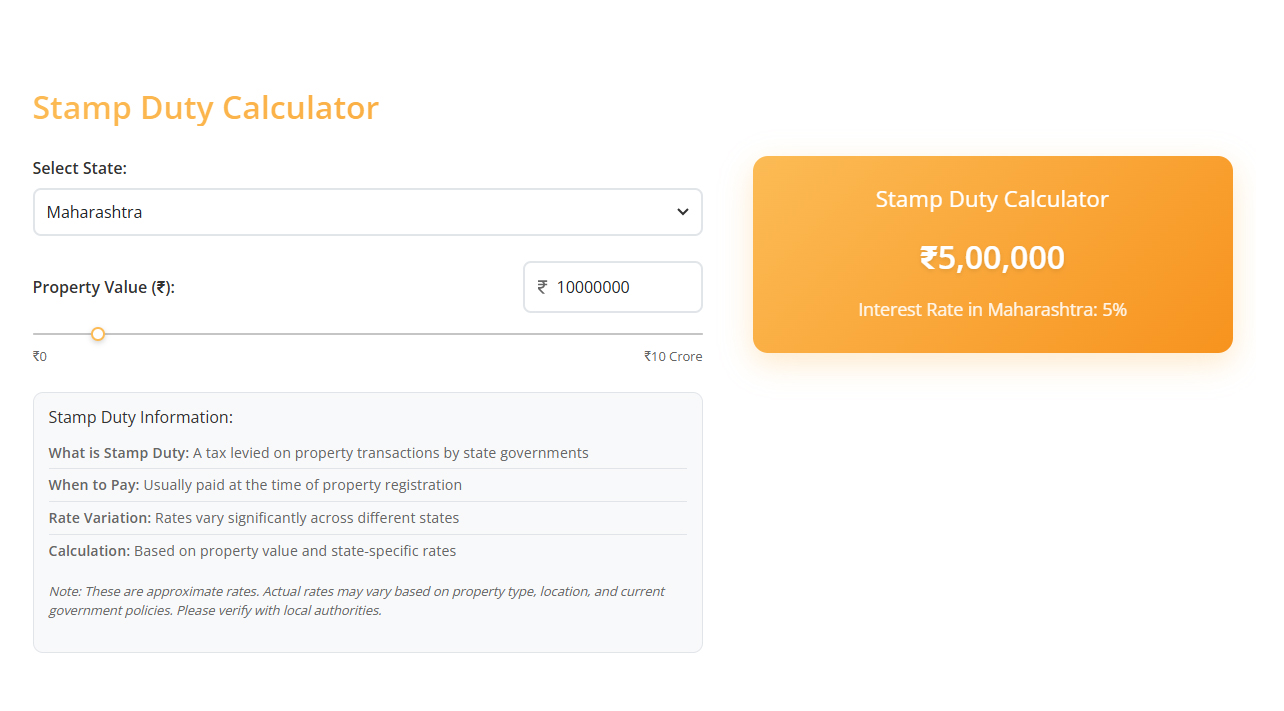

Hidden costs include stamp duty, registration charges, maintenance fees, property taxes, and occasional legal or documentation fees not included in the basic property price.

The process typically includes budgeting, searching for a property, conducting legal verification, applying for a loan, signing the agreement, completing registration, and taking possession. Each step ensures smooth and legal property acquisition.

Homebuyers can claim deductions under Section 80C for principal repayment (up to ₹1.5 lakh), Section 24(b) for interest on home loans, and additional benefits under Sections 80EE and 80EEA, depending on property type and eligibility.

It depends on financial flexibility, timeline, and risk tolerance. Ready-to-move properties offer immediate possession and fewer uncertainties, while under-construction homes may provide better pricing, schemes, and customisation options.

Verify the property title, approvals from local authorities, builder credibility, and compliance with RERA guidelines. Also, check encumbrance certificates and ensure there are no pending dues or disputes on the property.

Chennai

99629 44444

Coimbatore

72993 70000

Bangalore

98848 00062

Delhi

73388 66895

Hyderabad

73581 35136

Pune

82200 34547

Dubai

44205777

NRI

91763 44444